“Is it smart to close a credit card? If yes, when?” That’s the gist of emails I received recently from Brad, Jan, Sam, and Tony. Here’s what I do.

credit card? If yes, when?” That’s the gist of emails I received recently from Brad, Jan, Sam, and Tony. Here’s what I do.

I try out a lot of different cards. If I decide that I no longer want to keep a card after trying it out for a year, I do three things before cancelling.

- Call the number on the back of the card and ask if they will waive the annual fee for another year. If no…

- Ask if they have a free version of this card. Many do. That keeps the card’s credit history alive. If no…

- Ask if they will transfer the credit line to another card that I have at their bank. My experience is that they usually move all but $500 of the credit line. This keeps one’s current available credit limit amount over all your cards at their bank virtually the same – even if you cancel the card.

- If I strike out on all three options… only then do I cancel the card.

Why Not Just Cancel The Card?

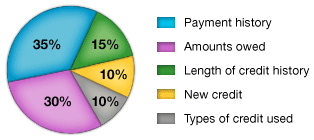

When I was a youngin’, I figured I was less of a risk if I had less available credit. I thought that made sense because I had less to not pay back! Alas, it can hurt your credit score if you cancel a credit card. Why? As you can see in the diagram here, 30% of your FICO credit score is based upon how much money you owe. AKA your Debt-To-Credit-Limit percentage.

When I was a youngin’, I figured I was less of a risk if I had less available credit. I thought that made sense because I had less to not pay back! Alas, it can hurt your credit score if you cancel a credit card. Why? As you can see in the diagram here, 30% of your FICO credit score is based upon how much money you owe. AKA your Debt-To-Credit-Limit percentage.

Let’s say you have two credit cards. You owe $1,000 on a credit card that has a credit limit of $2,000. You have a second credit card that has no balance on it and has a credit limit of $8,000. If you combine the amounts on the two cards, you owe $1,000 and have a credit limit of $10,000 ($2,000 + $8,000).

Right now, your Debt-To-Credit-Limit percentage is $1,000 divided by 10,000, or 10%. But if you cancel the card that has an $8,000 limit, you are left with one card. You owe $1,000 on that card and have a limit of $2,000. Now you have a Debt-To-Credit-Limit percentage of 50%.

Therefore, it is best to keep both cards around. Another reason, as you can see from the pie chart, 15% of your FICO score is your Length of Credit History. Keep those old cards around!

What About My Score?

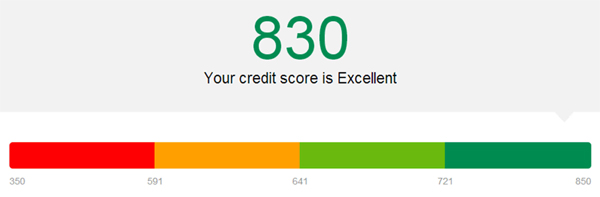

As far as cancelled cards not looking good on your credit record/report I would not worry about it. I can relate my personal experience to you. I just pulled my free Equifax credit score for owning a copy of Quicken 2015. My Equifax FICO credit score is 830. That is out of 850, so it’s pretty sweet! The report that accompanied my score shows that I have 59 accounts. 25 closed and 34 open. Most of those closed accounts are credit cards. The others are mortgage accounts from when I refinanced. I get new credit cards every year. I got 8 new cards in the past year. If I can’t downgrade to free versions, I usually cancel them.

Don’t Go Dormant – Gas It Up!

![]() I have a slew of cards that I don’t use regularly. Those are the no annual fee versions of cards to which I I downgraded over the years. One needs to put activity on those cards or they may go dormant, get cancelled and thereby lower one’s credit score.

I have a slew of cards that I don’t use regularly. Those are the no annual fee versions of cards to which I I downgraded over the years. One needs to put activity on those cards or they may go dormant, get cancelled and thereby lower one’s credit score.

My solution: I mark my calendar to do something every January. I swing by my safe deposit box, grab my cards and take them to the gas station. I fill up my tank by putting $2 on every card, and then return the cards to the safe deposit box. Then I wait a couple days to pay off all my cards in full online. Done and done. Some say that this needs to be done every six months to keep cards from going dormant. I have done it annually for several years without a problem.

If gas stations don’t work for you, you can always buy yourself e-gift cards at Amazon.com (click here). Load up your credit cards there and buy the eGift cards. That eGift card will show up in your Inbox momentarily. Click on the link in the email to load the eGift card to your account for future purchases.

Another option is to use the self-checkout at the grocery or be a Good Samaritan and feed some parking meters that take credit cards.

Great Bonuses, Batman!

There are some great sign-up bonuses out there right now. Chase Ink (50,000 points worth $500 in tax free cash), Chase Freedom ($225 in tax free cash), Delta Amex (50,000 miles), and Southwest (50,000 miles).

Click on “Chip’s Favorite Credit Card Offers” at the top right side of this website to get up-to-date info on this card. Email me if you have any questions. You don’t have to use my links, but I appreciate it when you do! That helps keep the 1s and 0s flying around cyber-space.